TFSA contribution limit

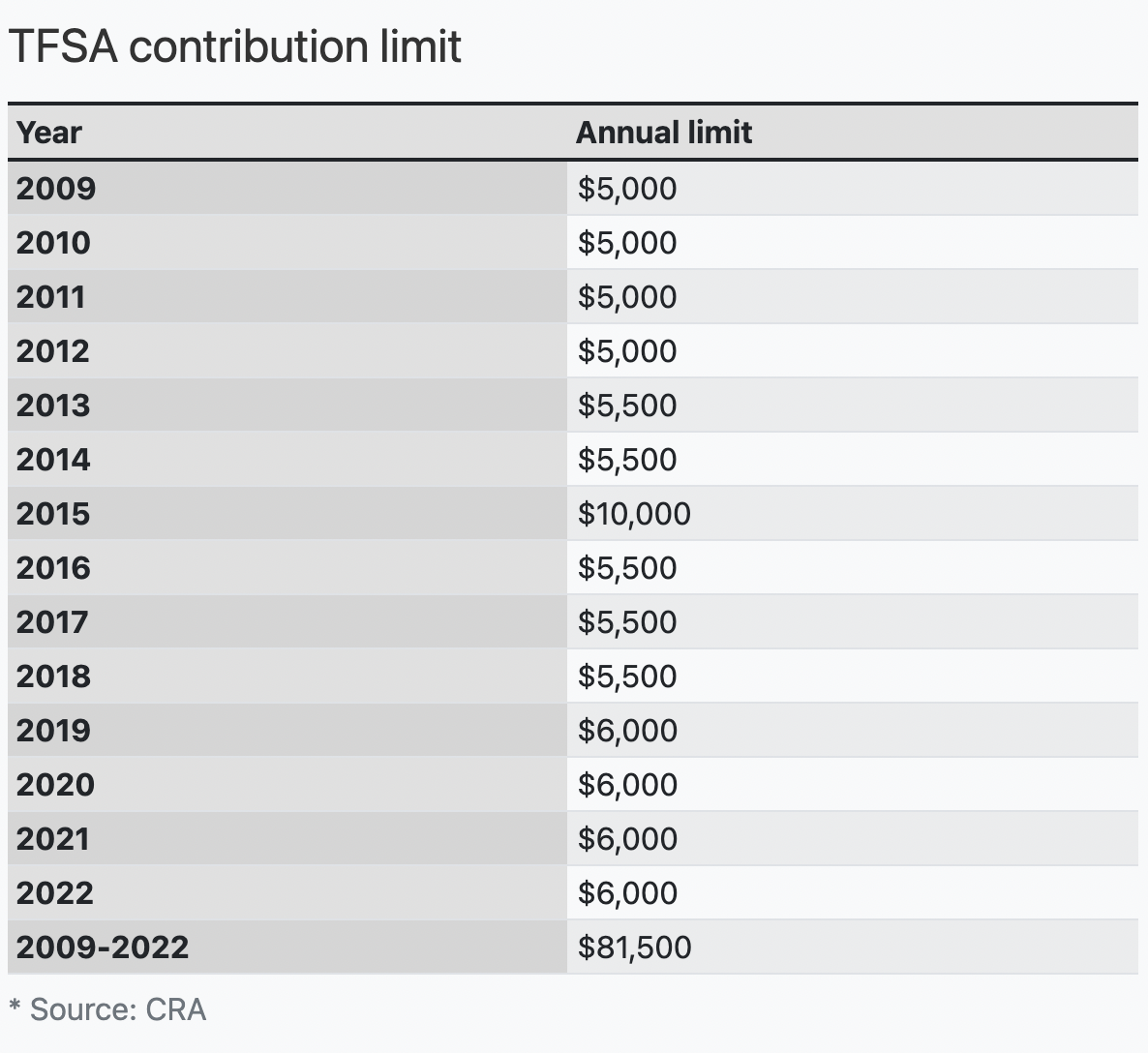

Your total cumulative TFSA limit increases every year from the year you turn 18. As of 2022, the total cumulative lifetime TFSA limit for Canadians who turned 18 before 2009 (the year TFSAs began) is $81,500.

The government sets a TFSA dollar limit for every year. The amount of the increase is indexed to inflation and rounded to the nearest $500.

For example, the annual TFSA limit is $6,000 for 2022, the same as for the years 2019 to 2021. From 2016 to 2018, it was $5,500.

A better online investing experience

Easy to use and powerful, Qtrade's online trading platform puts you in full control with tools and resources that help you make well-informed decisions.

Invest NowHow much can I put in my TFSA in 2022?

If you’ve been contributing every year you’re eligible, then it’s the remaining roll-over amount, plus $6,000.

The idea is that the unused TFSA contribution room can be used in following years. So if you only contributed $1,000 in 2021, you have $5,000 remaining. This means you can contribute $11,000 in 2022: last year’s $5,000 plus this year’s $6,000.

If someone who turned 18 before 2009 has never contributed to a TFSA, then they can dump the whole $81,500 at once, if they have the money. But this means they have reached their contribution limit.

How to find your TFSA contribution room

You can go to the CRA website and add up the limits for each year starting from 2009 or the year you turned 18, whichever comes later. Then subtract whatever you have already put into TFSAs. What remains is your available contribution room.

Your TFSA also appears on your notice of assessment from Canada Revenue Agency. This will show you your contributions, withdrawals and how much contribution room you have left.

There are also online calculators that can give you a rough estimate of how much room you have in case you didn’t max out your TFSA. But going the official CRA route is obviously the best way to go.

Grow Your Savings Effortlessly with Moka

Automate your savings with every purchase and watch your money multiply. Moka rounds up your transactions and invests the spare change. Start building wealth effortlessly today. Join thousands of Canadians embracing financial freedom with Moka

Sign up nowPenalty when exceeding the TFSA limit

Although you may want to deposit more, there are penalties for exceeding the TFSA contribution limit.

This extra amount is called the “TFSA excess amount,” and in order to avoid any penalties, TFSA users need to immediately withdraw it from their TFSA.

If you wait for more contribution room to absorb the excess in the following year, you will be faced with a penalty tax of 1% of the excess amount, payable for every month in which there is an excess. Those owing these penalty taxes have to file a special TFSA return (Form RC243) to calculate and report the taxes. June 30 of the following year is the deadline for filing the returns.

So try your best to avoid depositing any excess amount; it’s a headache.

You can use the TFSA as an emergency fund

Many compare TFSAs to the Registered Retirement Savings Plan (RRSP). However, the main difference is your earnings in a TFSA are protected from taxes when withdrawals are made. This makes the TFSA a great emergency fund. With an RRSP, you get a tax deduction for your contributions, but you pay tax on anything you withdraw.

You don’t have to choose between a TFSA and an RRSP

Many ask themselves if they’d be better off with a TFSA than an RRSP, or the other way around.

After all, the RRSP’s yearly contribution is a lot higher than the TFSA’s. For example, the RRSP contribution limit was $27,830 in 2021 and it was $27,230 for 2020. But withdrawals are taxed.

For that reason, the RRSP works much better for long-term savings goals, like retirement. After all, once people turn 71, they can no longer contribute to their RRSP and must convert it into a registered retirement income fund (RRIF) that they must withdraw from.

The idea stems from the notion that people will be in a lower tax bracket when they are retired than when they were working, so they will pay lower taxes on the money stashed in an RRSP.

The TFSA works better for medium- and short-term goals. A TFSA allows you to save and potentially grow investments – tax-free – for instance for a mortgage down payment, an emergency fund, or a car.

The TFSA has no withdrawal limits. Also, withdrawals do not count as income, meaning there will be no impacts on benefits like the GST Credit, Employment Insurance and Old Age Security.

And any money taken from a TFSA is added back to the TFSA contribution room the following year.

Sponsored

Trade Smarter, Today

With CIBC Investor's Edge, kick-start your portfolio with 100 free trades and up to $4,500 cash back.